Filing a corporate tax return incorrectly is not just an administrative inconvenience — it can result in penalties, interest charges, missed refunds, and in serious cases, reassessments that go back multiple years. Yet many incorporated business owners in Toronto file returns with errors or omissions that could have been avoided with proper guidance. Understanding the most common mistakes is the first step toward avoiding them. Professional assistance with corporate tax returns Toronto corporations rely on can help ensure accuracy, reduce compliance risks, and identify opportunities to optimize tax outcomes while staying fully aligned with CRA requirements.

Misclassifying Capital and Current Expenses

One of the most frequent errors is misclassifying expenses as either capital or current expenditures. The distinction matters because current expenses are fully deductible in the year they’re incurred, while capital expenditures must be depreciated over time using the CCA system. Incorrectly treating a capital item as a current expense inflates your deductions in the current year and creates problems if the return is ever reviewed. The reverse — treating a current expense as capital — means you’re understating your deductions and paying more tax than necessary.

The Importance of Professional Tax Guidance

Getting accurate help with corporate tax returns in Toronto businesses depends on means working with professionals who know these distinctions and apply them correctly across your entire expense base. That expertise extends to understanding which assets qualify for accelerated depreciation under the current incentive programs, which can meaningfully reduce taxable income in the year of purchase.

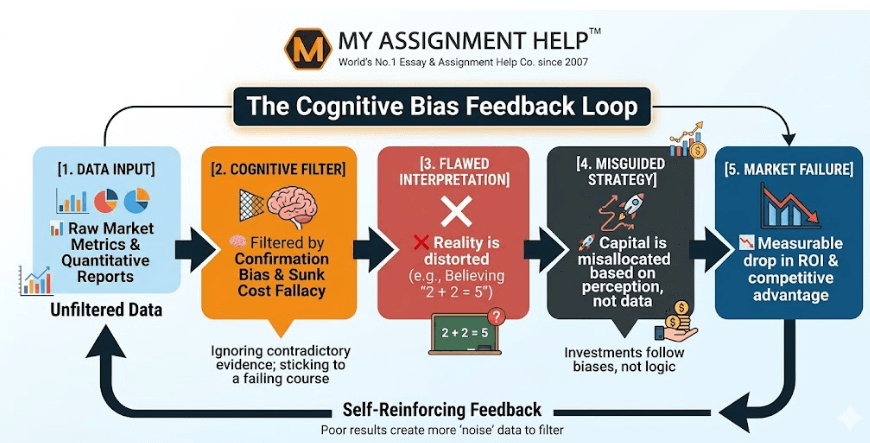

See also: Data vs. Perception: Navigating Logical Fallacies in Business Strategy

Managing Shareholder Loan Accounts Properly

Shareholder loan accounts are another area where errors are common and consequences are significant. If you borrow money from your corporation and don’t repay it within the required timeframe, the CRA deems the outstanding balance to be income in your hands — at your personal marginal rate. This rule exists to prevent indefinite tax deferral through shareholder loans, and it’s enforced rigorously. Tracking shareholder loan balances carefully and ensuring repayment within the prescribed period is essential.

Avoiding Late Filing Penalties

Failure to meet filing deadlines is not uncommon, especially for newly formed companies that are not yet aware of their corporate filing schedule. The deadline for filing the T2 is six months from the end of the fiscal year. If any tax is owed, it is supposed to be paid two months later (or three months later if the company qualifies as a CCPC). Failure to file results in an automatic penalty of 5%, plus 1% per month for up to 12 months.

Claiming Available Tax Credits

Failing to claim available credits is another costly oversight. The SR&ED credit, Ontario innovation tax credit, apprenticeship training tax credit, and various other incentives are available to qualifying corporations but require affirmative steps to claim. Many businesses leave these credits unclaimed simply because they don’t know they’re eligible or don’t have professional guidance that raises the question.

Handling Related Party Transactions Correctly

Related party transactions are a frequent source of CRA scrutiny. If your corporation pays rent to a related party, charges management fees to or from an associated corporation, or has any transactions with entities you’re connected to, those transactions need to be at fair market value and properly documented. Below-market transactions between related parties can be recharacterized by the CRA, resulting in adjustments and potential penalties.

Reporting All Sources of Corporate Income

Not reporting all income sources is an error that ranges from oversight to more serious territory depending on the circumstances. Corporations that receive income from multiple streams — product sales, consulting fees, investment income, rental income — must ensure all of it is reported. The CRA’s matching programs are increasingly sophisticated, and discrepancies between what third parties report paying to your corporation and what appears on your T2 are a reliable audit trigger.

Conclusion

The best way to avoid these and other corporate tax errors is to work with a qualified professional who understands the corporate tax system deeply, asks thorough questions about your business activities, and prepares returns with genuine attention to detail. The cost of professional preparation is almost always less than the cost of the errors it prevents, making expert support for corporate tax returns in Toronto businesses a valuable investment in both compliance and long-term financial success.